All U.S. businesses are marijuana related businesses (MRBs). By “all” I mean everyone from Amazon to your local hardware store, with very few exceptions. Allow me to explain.

Guidance on banking and MRBs

Over eight years ago, the Financial Crimes Enforcement Network published the FinCen Memorandum of February 14, 2014 (“FinCen Memo”). FinCen is a Bureau within the U.S. Department of Treasury. Its mission is to combat money laundering and financial crimes.

I’ve written that in cannabis years, the FinCen Memo is as old as dirt and reads like a relic of a bygone era. However, since companion guidance from the U.S. Department of Justice on “Marijuana Related Financial Crimes” was rescinded in 2018, the FinCen Memo has been the only game in town for federal banking guidance.

People often cite the FinCen Memo as creating the three “tiers” into which banks and credit unions triage MRBs for know-your-customer (KYC) and screening purposes. That’s wrong. The FinCen Memo doesn’t mention tiers at all. The closest we have to a federal framework is from this 2018 SBA Policy Notice, which categorizes MRBs as “direct”, “indirect”, and “hemp-related businesses.” But banks don’t really use that.

Instead, early industry adopters — like our pioneering credit union clients — began using a three-tiered system to analyze potential cannabis industry clients within the FinCen framework. I believe this system was first expounded in 2016 by Steve Kemmerling of CRB Monitor. It involved the following categories (I’ll paraphrase a bit):

- Tier I MRB: “Plant touching” businesses licensed by the state. Cannabis dispensaries, cultivators, processors and testing facilities all fall under this definition. These are the highest risk businesses for banks and constitute the majority of suspicious activity report (SAR) filings.

- Tier II MRB: Businesses that rely on Tier I MRBs for the majority of their revenues and play a large role supporting the industry. See: equipment suppliers, consultants and industry associations. These businesses are lower risk for banks than Tier I. However, banks target them for enhanced KYC.

- Tier III MRB: Businesses that service Tier I businesses, but do not rely on the cannabis industry for their primary source of revenue. Classic examples include lawyers, accountants, property management firms and utility companies.

These tiers were revised and further parsed by CRB Monitor in 2020, but in my experience, most financial institutions keep it simple with the legacy framework. It isn’t a legal framework, after all. It’s just an expedient model that has been adopted widely given the federal leadership vacuum.

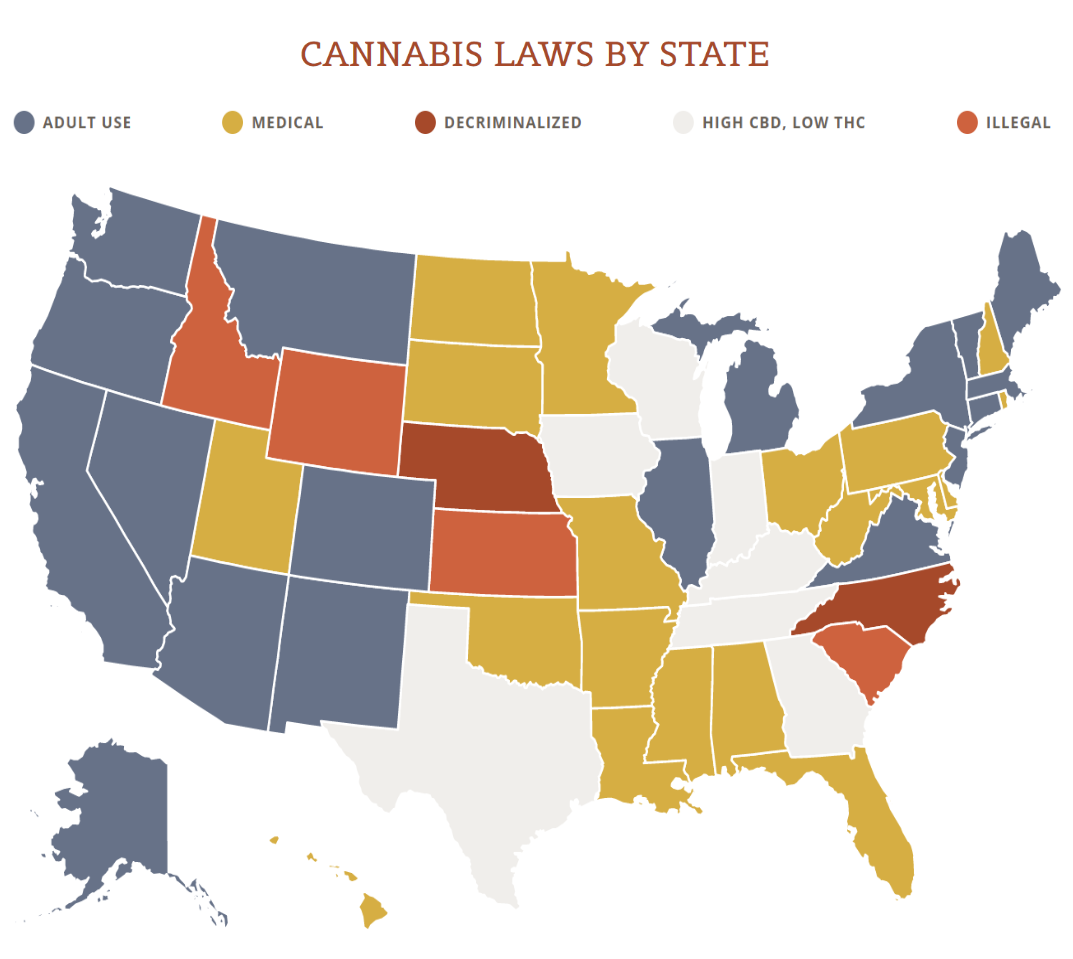

View the US Map of Marijuana Legality

All businesses are MRBs

Now, go read the Tier III MRB definition again. Do you know who it captures– beyond lawyers, accountants, etc.? It captures everyone. Everyone accepts Tier I MRB revenues, knowingly or otherwise. This includes the federal government itself, which collects billions of dollars from these businesses annually through IRS payments.

It’s worth digressing to note here that individuals are also staked financially to the cannabis industry, knowingly or otherwise. Do you own a 401K or mutual fund? Perhaps you own a small sliver of Innovative Industrial Properties, a cannabis REIT which is publicly traded on the New York Stock Exchange (NYSE). Or maybe you own a slice of Scott’s Miracle Gro, another NYSE company. Scott’s has one subsidiary that invests directly into the cannabis industry and another that has supplied hydroponics and gardening supplies directly to marijuana grows since 2015. In all, more than 145 million Americans now live in a state that has legalized marijuana. These individuals receive services funded with cannabis industry revenues– from schools to policing.

Legal cannabis sales in the U.S. are projected to top $30 billion this year. The cannabis industry is also the most prolific job creator in America, supporting more than 428,000 “legal” jobs. Given this entrenchment, vanishingly few businesses in America refuse to provide products or services to licensed cannabis businesses– with the prominent exception of banks. Even if a business wished to embargo MRB interactions, it would be very difficult to draw clean lines given how cannabis commerce is deeply woven into the fabric of the U.S. economy.

We all support MRBs and banking must be fixed

Financial institutions are banking MRBs knowingly or otherwise. When an industry gets this big, it’s simply unavoidable. The Tier III MRB designation should disappear, and in the bigger picture the need for banking reform is simply irrefutable. Maybe, just maybe, that will happen this year. The SAFE Banking Act is once again in the news this month, now bundled into larger legislation after clearing the House of Representatives five separate times. Until that happens, and maybe even after, banks, businesses and all of us will work with “MRBs.”